Table of Content

Domestic partners and fiancés are also eligible to give funds for a down payment. If your family decides to help you out with a down payment gift, you should be extremely happy. However, like any large financial move, there are some rules and regulations to consider. Perhaps the most important is for the giver of the gift, as they’ll need to account for that money on their taxes.

Neither FHAnewsblog.com nor its advertisers charge a fee or require anything other than a submission of qualifying information for comparison shopping ads. FHANewsBlog.com was launched in 2010 by seasoned mortgage professionals wanting to educate homebuyers about the guidelines for FHA insured mortgage loans. Popular FHA topics include credit requirements, FHA loan limits, mortgage insurance premiums, closing costs and many more. The authors have written thousands of blogs specific to FHA mortgages and the site has substantially increased readership over the years and has become known for its “FHA News and Views”. If you’re set on buying now, there are programs that offer down payment assistance and low down payment options, as well as programs for those with disability benefits.

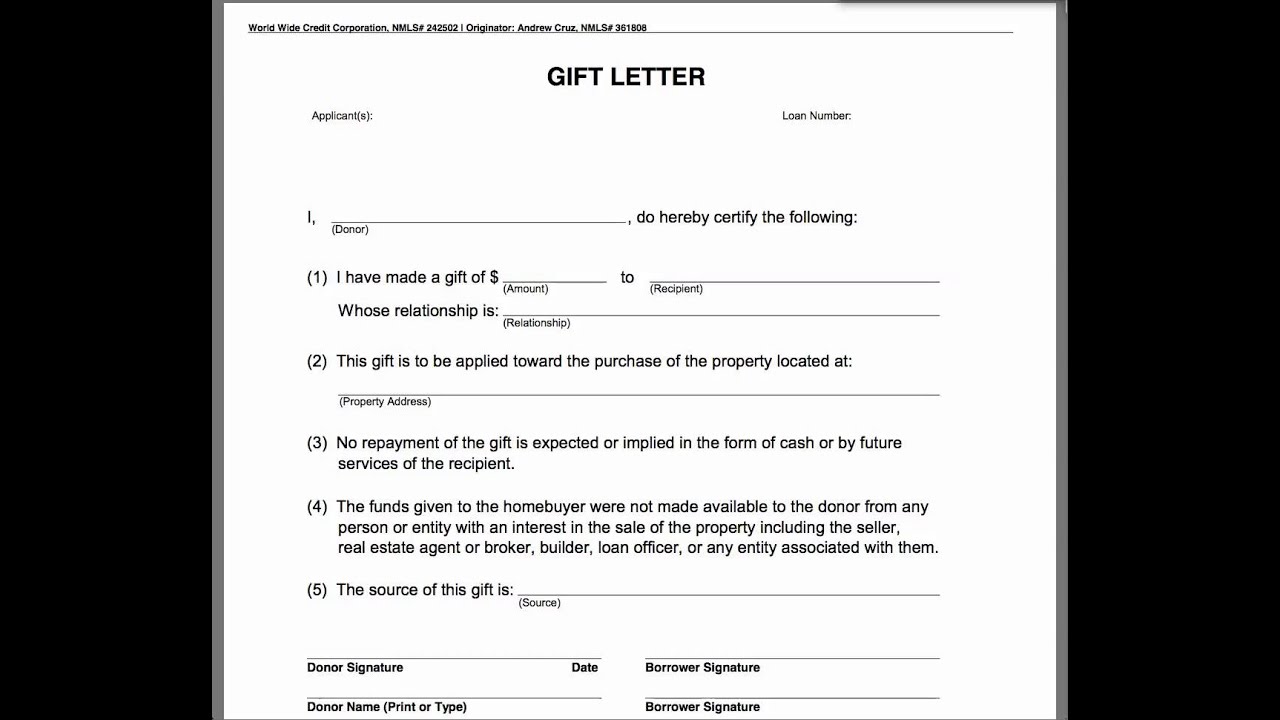

What is a Gift Letter for a Mortgage?

The contents required in the letter are generally simple and straightforward. The funds cannot come from payday loans, cash advances on your credit card, etc. Anyone helping you must also follow the same sourcing rules as you; no cash advances, payday loans, etc. VA loans are for qualifying military members, USDA loans are need-based.

There are rules that permit a borrower to receive such outside help, but the source and purpose of these funds are carefully regulated under FHA mortgage loan rules. That doesn't mean the agency doesn't provide resources that can help you locate a DPA program in your area. These programs must meet adhere to federal regulations when providing down payment help to borrowers. Those who have marginal FICO scores are required to make a 10% down payment. According to FHA home loan minimum standards, those with FICO scores between 500 and 579 are required to come up with this higher down payment. Those with FICO scores at 580 or higher technically qualify for the lowest down payment offered.

down improves mortgage rates

In the last months of 2022, the FHA and HUD issued a mortgagee letter announcing a crucial change in FHA loan approval policy. The FHA Single-Family Home Loan program was modified in 2022 to permit lenders to submit positive rental history as a factor in home loan approval. 3) Your rental history can help boost your credit if you pay on time and have a pattern of doing so. But the catch is that your landlord must report this activity to the credit agencies. You'll need a minimum of 12 months of on-time rent and utility payments; anything less can seriously hurt your chances for loan approval. What if you can't come up with the entire down payment on your own?

Many lenders will already have templates in place for their borrowers and additional parties involved, such as gift-givers. Repaying money that was initially documented as a down payment gift is considered mortgage fraud, which is a crime that can result in serious legal ramifications. Mistating gift funds can also put your loan qualification in jeopardy, as all forms of lending need to factor in your debt-to-income ratio. Even though lenders do allow gift funds, they also require mortgage applicants to disclose the source of these funds.

How to save for a down payment on a house

The amount you borrow with your mortgage is known as the principal. Each month, part of your monthly payment will go toward paying off that principal, or mortgage balance, and part will go toward interest on the loan. Do you know how your chosen FHA lender will calculate your down payment? Knowing before you apply can help plan and save for this and other required closing costs.

The funds can come from the borrower’s savings, cashed-in investments, gift funds from others , even down payment assistance . Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and, services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories. While we strive to provide a wide range offers, Bankrate does not include information about every financial or credit product or service. Browse through our frequent homebuyer questions to learn the ins and outs of this government backed loan program.

Check with your lender about what information they require in the gift letter. They may also provide you with a template letter to use or specific guidance as to how to best structure the letter. In this post, we cover all of those questions and other considerations to keep in mind when accepting a down payment gift for a mortgage, and how new homeowners should account for these funds. We're the Consumer Financial Protection Bureau , a U.S. government agency that makes sure banks, lenders, and other financial companies treat you fairly. In the beginning, you owe more interest, because your loan balance is still high. So most of your monthly payment goes to pay the interest, and a little bit goes to paying off the principal.

In some instances, though, your family may decide to gift you some money towards a down payment. This will work wonders over the life of your loan, as a larger down payment equals less money in interest. You may want to talk to a financial advisor about a down payment gift before you make on, though. First-time buyers want to know how much they're expected to save for their FHA loan down payments.

Beyond that amount, the funds must be reported on the donor's gift tax return. In turn, parents can collectively give up to $32,000 per child without needing to report those funds to the IRS. The content on this page provides general consumer information. This information may include links or references to third-party resources or content. We do not endorse the third-party or guarantee the accuracy of this third-party information. Down payments are due as part of your cash to close; you cannot finance the down payment or otherwise not make the payment in your cash to close.

The lender arrives at an amount for the adjusted value of the property based on the results of the FHA appraisal, which is one reason why appraisals are required for new purchase home loans. How much money you’re eligible to receive as a down payment gift depends on the type of mortgage you’re borrowing. If you’re taking out a standard conventional loan, all of your down payment can be gifted if you’re putting down 20% or more. If you’re putting down less than that, part of the money can be a gift. However, some of it will probably have to come out of your own pocket, with the final split varying based on your loan type.

Our experts have been helping you master your money for over four decades. We continually strive to provide consumers with the expert advice and tools needed to succeed throughout life’s financial journey. Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions.

This is why a lender will ask for copies of your most recent bank statements. The purpose of reviewing your bank statements is to ensure you have enough in reserves for mortgage expenses. But sometimes, a family member offers to pay these expenses as a gift to you.

The down payment on a house is a portion of the price of a home that’s paid in cash. The balance of the purchase price is usually paid by a loan you secure from a lender and pay back in a monthly mortgage payment. Down payments are expressed as a percentage of the total purchase price. The percentage you’re required to pay is dictated by the terms of your loan. Note that not all home buyers with financing are required to produce a down payment, but the majority of them are.

The posted content contained on FHAnewsblog.com is for general information purposes only and is accurate and true to the best of our knowledge. The information should not be seen as financial advice and you should consult with a licensed mortgage professional , prior to taking any action. FHAnewsblog.com assumes no responsibility for errors or omissions in the contents on the Service. Borrowers with FICO scores that fall below 579 are required, according to FHA loan rules, to pay more money down.

No comments:

Post a Comment